Company Car vs Salary Sacrifice vs Car Allowance

Providing employees with a vehicle is one of the most popular employment benefits in the UK. However, there are three very different ways an employer can help an employee access a vehicle:

- Company Car

- Salary Sacrifice Car Scheme

- Car Allowance

Although these options all help employees access a vehicle, they are taxed very differently and can have significantly different costs for both the employer and employee.

This guide explains how each option works, how tax is calculated, and the advantages and disadvantages of each. For the purposes of this guide, we will assume the vehicle is valued at £50,000

Company Car

A company car is a vehicle that is purchased or leased by an employer and made available to an employee as part of their remuneration package. In most cases, the employee is permitted to use the vehicle for business journeys, travel between home and work, and private use, such as shopping, holidays and other personal trips. As the vehicle is available for private use, HMRC treats it as a Benefit in Kind (BiK).

How Tax on Company Cars Work

Employees are taxed on the Benefit in Kind.

The taxable benefit is calculated by multiplying the car's P11D value (its original list price) by the applicable BiK percentage, which is based on the vehicle's CO₂ emissions.

P11D Value × BiK Percentage = Taxable Benefit

The employee then pays Income Tax on the taxable benefit (but no National Insurance Contributions) at their marginal tax rate, while the employer pays Class 1A National Insurance on the benefit.

Example: Electric Vehicle

Vehicle P11D Value: £50,000

Vehicle CO₂ Emissions: 0g/km

BiK Rate (2026/27): 4%

Taxable Benefit: £50,000 × 4% = £2,000

Income Tax on the Taxable Benefit - depending on the employee’s marginal rate - is as follows:

| Income Tax Rate | Annual Tax | Monthly Tax |

|---|---|---|

| 20% | £400 | £33.33 |

| 40% | £800 | £66.67 |

| 45% | £900 | £75 |

Example: Petrol Vehicle

Vehicle P11D Value: £50,000

Vehicle CO₂ Emissions: 135g/km

BiK Rate (2026/27): 33%

Taxable Benefit = £50,000 × 33% = £16,500

Income Tax on the Taxable Benefit - depending on the employee’s marginal rate - is as follows:

| Income Tax Rate | Annual Tax | Monthly Tax |

|---|---|---|

| 20% | £3,300 | £275 |

| 40% | £6,600 | £550 |

| 45% | £7,425 | £618.75 |

What Costs Does the Employer Cover?

When a vehicle is provided through a company car scheme, the employer (or leasing company acting on its behalf) will usually cover:

- Vehicle lease or purchase costs

- Vehicle registration fee (first registration fee)

- Number plates

- Vehicle Excise Duty

- Delivery charges

- Servicing and maintenance (depending on the scheme)

- Insurance and Breakdown cover (depending on the scheme)

Salary Sacrifice Car Scheme

A salary sacrifice scheme allows an employee to exchange part of their gross salary in return for a company car provided by their employer. The employer purchases or leases the vehicle and remains the owner or lessee, while the employee agrees to reduce their contractual gross salary before Income Tax and National Insurance Contributions (NICs) are calculated. As with a traditional company car, if the vehicle is available for private use, HMRC treats it as a Benefit in Kind.

How Tax on Salary Sacrifice Cars Works

As the salary is reduced before Income Tax and National Insurance Contributions are calculated, the employee pays less tax and NICs on their salary.

For example, an employee earning £65,000 per annum gross salary, could choose to sacrifice £600 per month (£7200) in exchange for a company car, reducing their per annum gross salary to £57,800. This would mean paying less Income Tax and NI.

The Benefit in Kind is then calculated in the same way as a standard company car:

P11D Value × BiK Percentage = Taxable Benefit

The employee then pays Income Tax on the taxable benefit (but no National Insurance Contributions) at their marginal tax rate, while the employer pays Class 1A National Insurance on the benefit.

Example: Electric Vehicle

Gross Salary: £65,000

Net Salary: £48,257 (Example figure, only considering deductions for Income Tax and NI)

Salary Sacrifice: £600 per month (£7,200 per year)

Revised Gross Salary: £57,800

Revised Net Salary: £44,081 (Example figure, only considering deductions for Income Tax and NI)

Vehicle P11D Value: £50,000

Vehicle CO₂ Emissions: 0g/km

BiK Rate (2026/27): 4%

Taxable Benefit = £50,000 × 4% = £2,000

Income Tax on the Taxable Benefit – depending on the employee's marginal rate – is as follows:

| Income Tax Rate | Annual Tax | Monthly Tax |

|---|---|---|

| 20% | £400 | £33.33 |

| 40% | £800 | £66.67 |

| 45% | £900 | £75 |

Example: Petrol Vehicle

Vehicle P11D Value: £50,000

Vehicle CO₂ Emissions: 135g/km

BiK Rate (2026/27): 33%

Taxable Benefit = £50,000 × 33% = £16,500

Income Tax on the Taxable Benefit - depending on the employee’s marginal rate - is as follows:

| Income Tax Rate | Annual Tax | Monthly Tax |

|---|---|---|

| 20% | £3,300 | £275 |

| 40% | £6,600 | £550 |

| 45% | £7,425 | £618.75 |

It is important to note that by reducing and employee’s gross salary through a salary sacrifice scheme, you could be reducing the level of cover of an employer's death in service life insurance. This is because it is usually based on contractual gross salary.

What Costs Does the Employer Cover?

When a vehicle is provided through a salary sacrifice scheme, the employer (or leasing company acting on its behalf) will usually cover:

- Vehicle lease or purchase costs

- Vehicle registration fee (first registration fee)

- Number plates

- Vehicle Excise Duty

- Delivery charges

- Servicing and maintenance (depending on the scheme)

- Insurance and Breakdown cover (depending on the scheme)

Car Allowance

A car allowance is completely different. The allowance is treated exactly like salary.

Rather than providing a vehicle, the employer simply gives an allowance for the employee to use to help fund their own vehicle.

Under this option the employee:

- Purchases or leases their own vehicle.

- Arranges insurance.

- Pays for servicing and repairs.

- Pays road tax.

There are no Benefit in Kind calculations.

Example: Car Allowance

An employee earning £51,000 per year receives a £6,000 annual car allowance, increasing their taxable salary to £57,000. As the allowance is treated as ordinary earnings, it is subject to Income Tax and National Insurance in the same way as salary. For higher-rate taxpayers, this means a significant proportion of the allowance may be deducted through tax and National Insurance before it is received.

| Salary | Car Allowance | Additional Tax & NI Contributions |

|---|---|---|

| £40,000 | £6,000 | £1,680 (20% Income Tax + 8% NIC's |

| £51,000 | £6,000 | £2,520 (40% Income Tax + 2% NIC’s) |

| £130,000 | £6,000 | £2,820 (45% Income Tax + 2% NIC’s) |

Business Mileage

If employees receiving a car allowance use the vehicle for business travel, the employer can reimburse business mileage.

HMRC's Approved Mileage Allowance Payments (AMAPs) are currently:

| Vehicle | First 10,000 Business Miles | Over 10,000 Business Miles |

|---|---|---|

| Cars and Vans | 55p | 25p |

| Motorcycles | 24p | 24p |

| Bicycles | 20p | 20p |

If the employer pays less than the approved rates, the employee may be able to claim Mileage Allowance Relief from HMRC.

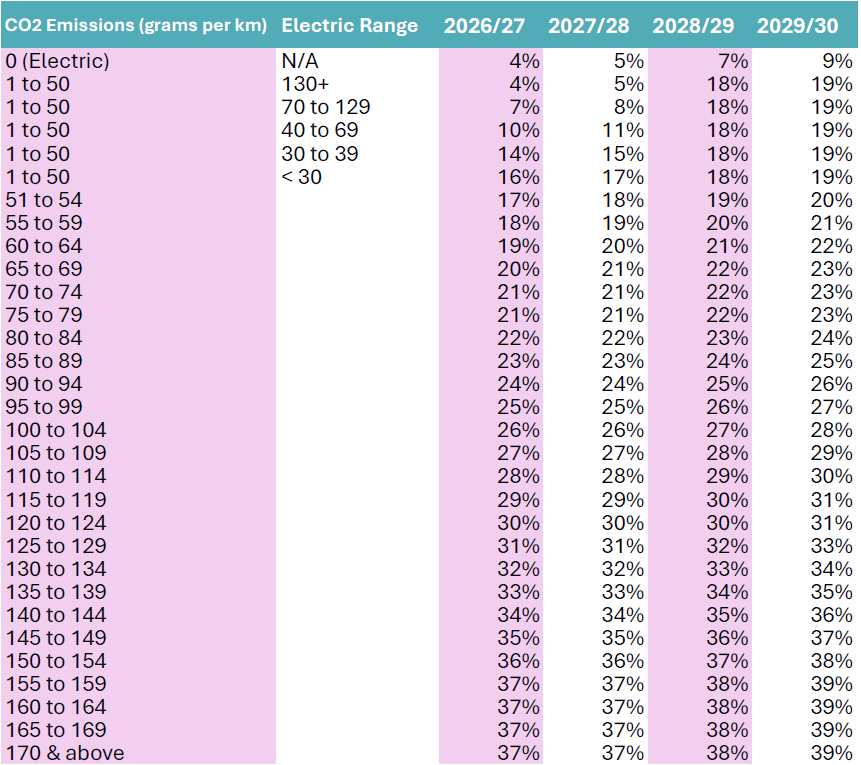

Benefit in Kind Rates for Electric, Hybrid, Petrol and Diesel Vehicles

For the 2026/27 tax year, the Benefit in Kind (BiK) rates for petrol and diesel company cars are based primarily on the vehicle's WLTP CO₂ emissions. Diesel cars that do not meet the RDE2 emissions standard are subject to a 4% diesel supplement, although the total BiK percentage is capped at 37%.

Can a Company Car Be Used Solely for Personal Use?

There is no legal requirement for a company car to be used for business purposes.

If a company provides a vehicle that is available solely for an employee's private use, it is still a company car for tax purposes.

HMRC taxes the availability of the vehicle for private use, not how much business mileage it undertakes.

Corporation Tax Relief for the Company

While a company can provide a vehicle that is used primarily or exclusively for private journeys, the tax treatment for the business is separate from the employee's Benefit in Kind position. Whether the company can claim corporation tax relief on the costs will depend on the specific circumstances and the applicable tax rules, so professional advice should be sought where a vehicle has little or no business use.

Second-Hand Company Cars

Many people assume buying a second-hand company car reduces the employee's tax bill. However, it does not as the Benefit in Kind is calculated using the vehicle's original P11D value, not what the employer paid.

The financial saving belongs to the employer through the lower purchase price.

Which Car Scheme Option is Best?

The most suitable option will depend on the needs of both the employer and the employee, as each has its own advantages and disadvantages.

A traditional company car offers convenience, with the employer typically covering many of the costs associated with the vehicle, with electric company cars providing significant tax savings through low Benefit in Kind rates.

Salary sacrifice schemes are often the most tax-efficient choice for employees looking to drive a new electric vehicle, as they can reduce both Income Tax and National Insurance liabilities.

A car allowance, on the other hand, provides employees with the greatest flexibility to choose and own their own vehicle, although it is generally less tax-efficient because it is treated as ordinary salary.

Before deciding which option is most appropriate, it is advisable to compare the costs and tax implications for both the business and the employee.

If you'd like to discuss these options for your business, you can get in touch with our team by phone, on 0121 633 2000, by email at enquiries@friendpartnership.com or by completing the form below with your query.

Make An Enquiry

Friend Partnership is a forward-thinking firm of Chartered Accountants, Business Advisers, Corporate Finance and Tax Specialists, based In The UK

Share this page: